Yet Another Overview of an AD System

My earlier article An Overview of an AD System introduced the basic responsibilities and principles of various modules (retrieval, ranking, bidding, cold start, etc.) from a technical perspective. Several years have passed, and while that understanding hasn’t become outdated, after experiencing more business operations, I’ve gained a more comprehensive view of the overall commercialization. This article attempts to understand an advertising system from another, more systematic perspective.

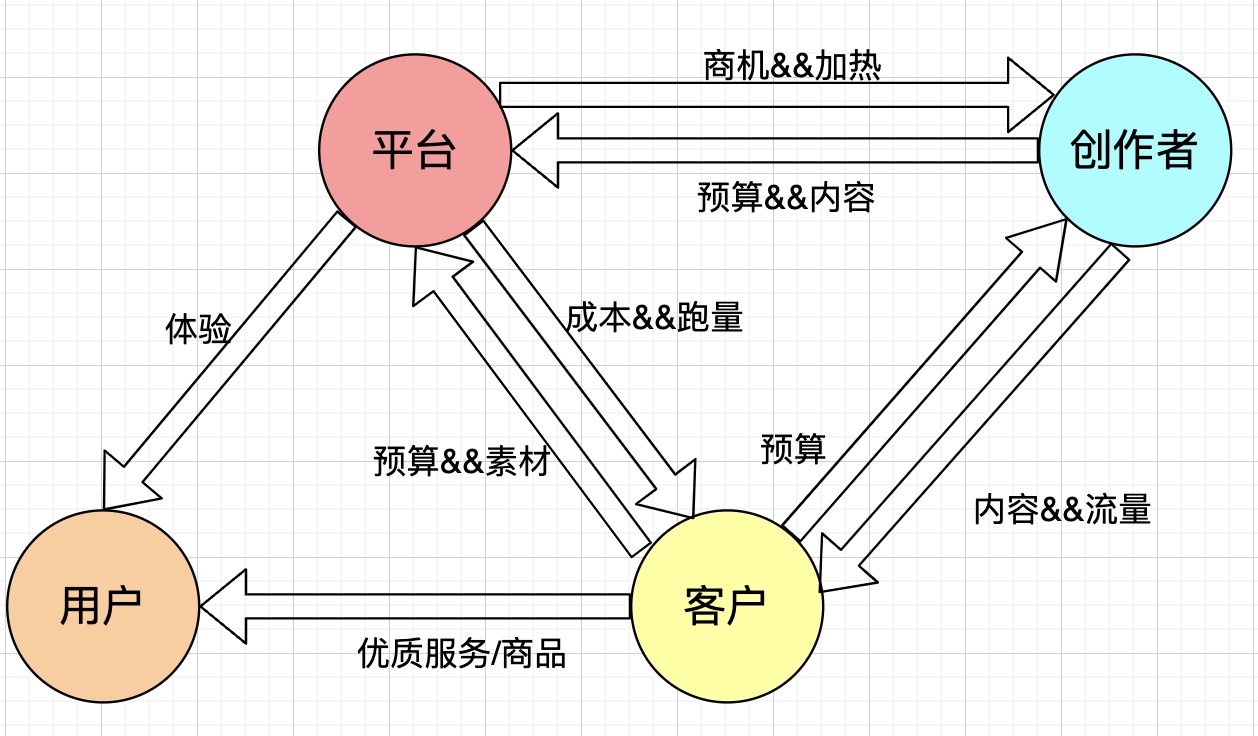

The traditional understanding of an ad system typically involves three parties: advertisers/agencies, the platform, and users. However, with the rapid development of content platforms (such as Douyin, Kuaishou, Xiaohongshu, Bilibili, etc.), more and more UGC content has emerged, making creators’ influence in commercial monetization increasingly difficult to ignore. Therefore, a fourth party representing creators has been added to the traditional three-party model, as shown below.

The complex relationships among these four parties generally exist on “first-party traffic” (borrowing the concept of first-party data), referring to platforms like Douyin/Kuaishou/Xiaohongshu/Bilibili that have the capability to build their own monetization teams and monetize on their own traffic. In contrast, “third-party traffic” scenarios generally only need to focus on the relationship between clients and the platform. A typical example is alliance scenarios (Chuanjia, Youlianghui, Kuaishou Alliance, etc.), where there are no strong user experience constraints on the user side because alliances are essentially traffic reselling businesses. The related technology is similar to first-party traffic, but there’s minimal attention to C-end user experience and creator aspects.

This article focuses on first-party traffic. The following content will discuss each party’s responsibilities and relationships with other parties according to the four parties mentioned above. The content will be somewhat scattered, but I hope you find it worthwhile.

The arrows in the diagram above can be understood as objectives that one party needs to deliver to another party. Taking the platform as an example, as the hub connecting all parties, the platform needs to fulfill the following responsibilities:

- For users, it needs to ensure that marketing content causes user experience loss within a red line, typically quantified as DAU loss. Common load constraints, frequency capping, negative feedback strategies, and hard constraints during mixed ranking are all attempts to optimize this aspect. The commercialization goal is to maximize commercial revenue within the DAU loss red line.

- For clients (advertisers), this is the platform’s key focus because clients are the platform’s revenue source. In short: after clients express their budget and creatives, the platform needs to maximize delivery volume under agreed cost constraints. To serve clients more precisely, the platform also segments by industry (e-commerce, gaming, education, etc.) and client type (KA, SMB) for optimization, providing richer marketing objectives and better delivery experience, creating better soil for clients’ long-term operations on the platform.

- For creators, the platform needs to provide monetization opportunities for creators (facilitating creator-client collaboration through official collaboration platforms like Xingtu, Pugongying, Juxing, Huahuo). The platform also needs to consider various issues (creator ecosystem, content ecosystem, underwater problems, etc.) in this process. At the same time, it must consider creator growth, providing mechanism strategies, various traffic heating tools (paid or free), and correspondingly, creators need to create good content for the platform.

Platform

As mentioned earlier, as the hub connecting all parties, the platform shoulders various responsibilities: experience (C-end and B-end), monetization (platform and creators), ecosystem (clients, creators, and content), and needs to deliver corresponding business metrics to all parties.

Experience: C-end and B-end

Based on user classification, experience can be divided into C-end users and B-end advertisers.

The experience the platform needs to deliver to C-end users is user experience. The most direct measurement metric is DAU loss, meaning users should not leave due to excessive marketing content or content that doesn’t match their interests. Technical approaches include load constraints, frequency capping/negative feedback/population-based strategies, or hard constraints during mixed ranking (ad first position, min-gap, etc.). These are all attempts to optimize this aspect, which will be expanded in the User section below.

The experience the platform needs to deliver to B-end is advertiser experience. The direct measurement metric is typically advertiser NPS surveys, but this metric often can’t be directly optimized. Issues like plan launch, delivery drop, volume, cost, and system variance all affect advertiser experience, directly or indirectly influencing advertiser NPS and long-term budget on the platform. Solving these problems can potentially improve B-end user experience. The cost issue is fundamental and most important, often guaranteed by CTR and CVR estimation accuracy, with “bidding + billing” as fallback. Additionally, there are stability initiatives for plan delivery drops and volume fluctuations, cold start initiatives for plan launch issues, etc.

As mentioned earlier, the commercialization goal roughly speaking is to maximize commercial revenue within the red line constraint of C-end user experience damage. C-end user experience has relatively clear measurement metrics: ad load and DAU loss. The former is easy to measure, while the latter often has poor observability, requiring very long observation periods. Often, correlated intermediate metrics like duration are used for direct optimization, but the overall optimization direction is relatively clear.

For B-end advertisers, there’s no directly measurable metric. NPS might count as one, but it’s not a directly optimizable metric. Therefore, advertiser experience is often split into several directions: launch (accelerating plan launch through cold start support), delivery drop (identifying and supporting drops), system variance (plan copying and pruning), cost (correction and bidding), etc. Delivering these experiences ultimately aims to get B-end advertisers to invest more budget long-term on the platform.

Monetization: Platform and Creators

Monetization is also divided into two parts: platform monetization and creator monetization. Platform monetization is the conventional ad monetization by selling traffic. Creator monetization refers to creators earning compensation by creating good content for clients or the platform, which has gradually emerged as a direction during the development of content platforms in recent years.

- Platform Monetization

Platform monetization, i.e., ad monetization, often requires doing three things well. Many internet companies also build organizational structures based on these directions (ranking group, traffic group, industry group).

1. Ranking Efficiency: Improving ranking efficiency in the pipeline, such as model AUC and pipeline consistency.

2. Traffic Mechanism: Clarifying ranking formulas and auxiliary strategies in the pipeline to meet traffic delivery objectives (spend, experience, ecosystem, etc.).

3. Client Products: Various advertiser products serving client needs (marketing objective diversity, cost, volume, low-barrier delivery, data privacy, etc.). This part will be expanded in detail in the Client section.

From a technical principle perspective, these things are all about maximizing platform matching efficiency, or traffic selling efficiency. Because fundamentally, revenue = cpm × ad_load. Ad_load is basically a fixed value (although there are many indirect ways to expand load like universal delivery), so the technical optimization direction is CPM growth. If we roughly decompose CPM, we can consider cpm ≈ bid × ctr × cvr. To improve CPM, we need to consider each of these factors separately: bid, ctr, cvr.

- Factor 1: bid

Looking at bid first, intuitively this is the average bid level for competitive traffic. For most oCPX ads, this bid is also often the advertiser’s average bid level (for nobid products, there’s no advertiser bid, but bid can still reflect advertiser budget to some extent). The system cannot raise bid without constraints on the advertiser’s bid basis because the advertiser’s bid expresses their expectation of conversion cost. If bid keeps increasing, cost can’t be well guaranteed. So this bid can basically be understood as “the price an advertiser is willing to pay for a conversion on a certain media platform”. Many factors affect the bid level an advertiser sets, with two key factors discussed here:

- Advertiser’s Business Model: A key factor is whether a conversion has value beyond that single conversion for the advertiser.

General white-label merchants’ budgets are pure performance budgets with strict ROI requirements. In this case, the price advertisers are willing to pay is relatively fixed across different media. In contrast, pure brand budgets have basically no strict conversion requirements. GD often involves premium traffic buying, where advertisers bid based on platform influence or traffic value.

In reality, many budgets fall between pure performance and pure brand budgets. So when advertisers bid, they adjust based on whether platform conversions bring spillover value. For example, advertisers on planting platforms like Xiaohongshu can accept costs for likes, saves, and follows that are higher than competitors like Douyin and Kuaishou, because advertisers believe a conversion on planting platforms brings more spillover value.

- Platform Competition Intensity: Whether advertisers can compete intensely on the platform.

On a media platform, if competition isn’t intense, in the most extreme case with only one advertiser, the pricing power for conversions is basically in that advertiser’s hands (which is also one of the problems the advertiser ecosystem needs to solve). When the number of advertisers increases, blue ocean becomes red ocean. Advertisers still have incentive to lower their profit margin and raise conversion bid costs for marketing, as long as overall ROI remains positive.

Therefore, assuming advertiser bids are rational, to raise the bid in the formula, the platform needs to increase its traffic value long-term (a somewhat abstract concept related to market recognition and influence), satisfy more advertiser marketing needs, introduce more advertisers to the platform, and create a healthy competitive environment. This is mainly handled by the third part mentioned above (client products), though also involving the first part (CTR/CVR estimation accuracy) and second part (traffic strategies affecting advertiser ecosystem).

- Factor 2: ctr × cvr

The other two factors are CTR and CVR. Since they’re similar, I’ll discuss them together. Multiple factors affect improving CTR and CVR, with two key ones:

- The first that comes to mind is model ranking efficiency. The model’s job is to select items with highest CTR and CVR for users when they arrive. So improving model AUC should theoretically bring CTR and CVR improvement.

But in practice, ad system ranking formulas aren’t simply CTR or CVR maximization. They’re often ecpm + hidden_cost, where ecpm=bid × ctr × cvr is revenue maximization, and hidden_cost contains various terms to satisfy objectives beyond revenue (like cold start, delivery drop issues). Therefore, improving model AUC doesn’t necessarily bring final CTR and CVR improvement, because the ranking formula isn’t determined solely by CTR and CVR (for instance, items with lower CTR/CVR but sufficiently high bid could rank first overall).

But overall, long-term model iteration should bring posterior CTR and CVR increases. Because for advertisers, using low CTR/CVR creatives with high bids isn’t a sustainable approach, and the platform doesn’t advocate this (the platform guides advertisers to create good creatives). Therefore, for advertisers, improving CTR/CVR by making good creatives to get volume is a more sustainable approach.

- Another important factor is creatives. Creative quality directly affects metrics like user click rate and conversion rate. We need to increase supply of high-quality creatives, for example through matching platforms letting K provide more high-quality creatives for B, or using AIGC to generate more quality creatives. The platform can then combine model ranking efficiency and creative selection to improve overall CTR and CVR. For platform-side actions, see Dynamic Creative Optimization in Online Display Advertising and A Hybrid Bandit Model with Visual Priors for Creative Ranking in Display Advertising.

This part is mainly supported by the first part above (model efficiency) and second part (ranking formula, hidden_cost composition).

- Creator Monetization

Creators have developed along with content platforms and are now an important component of ad systems, shouldering the responsibility of creating good creatives. Related to this is the big topic of creator monetization, since creators can’t simply “create with love” but need stable income to support content creation.

There are many ways for creators to monetize, including from B-end (like commercial orders, livestream sales), from platform (like platform subsidies), from C-end (like livestream gifts, charging). See Bilibili Creator Monetization Introduction.

Commercial orders from B-end are the most common method. Clients (hereafter B) find creators (hereafter K) to write promotional content. This is a typical matching process. Many content platforms have established official platforms (Xingtu, Pugongying, Juxing, Huahuo) to facilitate B-K collaboration. When B goes through official platform reporting, besides providing fixed-price or performance-based settlement (based on conversion count) for K, B also needs to provide a certain percentage commission to the platform. This content is called “above-water content”.

But besides “above-water content”, quite a bit of content goes “underwater”, meaning B and K don’t go through the official platforms mentioned above but reach collaboration directly. B has incentive to do this because the most direct benefit is no extra commission payment, and the content is more native-like UGC (some platforms require marking for content that went through matching). But for the platform, it definitely wants all content to go through official collaboration platforms, for the commission and to have understanding and control capability over K’s created content, including understanding K monetization industries, follower distribution, and influencing K’s content creation direction by affecting K’s opportunity distribution.

Therefore, regarding creator monetization, the platform’s vision is often: (1) more creators can monetize on the platform (through above-water methods), meaning monetization population and matching transaction volume continue to grow (2) contribute good content to the platform.

And in this process, a big problem the platform needs to solve is “converting underwater to above-water”, i.e., how to get more B-side budget to go above-water. This will be emphasized in the Creator section below.

Besides from B-end, platform subsidies are also a source of creator monetization. Common subsidies include cash and traffic. Many content platforms have creator incentive programs, settling with creators based on content play count or view count. There are also traffic supports like traffic coupons, traffic support for works under specific topics, etc.

Ecosystem: Clients, Creators, and Content

Ecosystem issues generally need consideration only after a platform reaches a certain scale. This ecosystem refers to non-red-line ecosystem issues, meaning issues that won’t cause platform failure if they appear (like politically sensitive topics). Instead, these are issues where short-term neglect shows no obvious problems, but long-term neglect is unfavorable for sustainable platform development, like plan cold start, advertiser diversity, creative diversity, creator monetization distribution, etc.

This is a typical scale-ecosystem problem. When scale is small, these issues aren’t significant, or growth is the most important point at that stage. But when scale becomes large, inevitably unhealthy problems appear. Colloquially, “when the forest gets big, all kinds of birds appear”, so ecosystem issues can’t be ignored.

- Client Ecosystem

Common client ecosystem issues include: client structure (like ratio of large to small advertisers, advertiser industry distribution), client operation habits (like frequent bid changes, plan copying, minor creative modifications, etc.).

As mentioned earlier, in the most extreme case with only one advertiser on the platform, traffic pricing power is in that advertiser’s hands. So the platform definitely wants to increase advertiser diversity, letting overall CPM level rise through advertiser competition.

But ad systems often have Matthew effect, where most money is spent by a small portion of advertisers. The reason is many long-tail small and medium advertisers can’t compete well with large advertisers due to weaker competitive ability and less delivery experience. These advertisers face further problems in the delivery pipeline due to sparse data and insufficient model learning, further exacerbating this issue. The platform needs to do specific optimization for these small and medium advertisers, establishing corresponding SMB initiatives. Some methods will be detailed in the Client section.

Another common client ecosystem issue is client delivery operation problems. For example, frequent bid changes. In normal oCPX ads, advertiser bid is their expectation of conversion cost, which should theoretically be fixed. Though adjustments may occur during initial delivery when there’s no fixed cost expectation (for instance, cost for a like differs across platforms, so advertisers need to adjust when switching platforms), but such changes shouldn’t be frequent. So frequent bid changes are often advertisers hacking the platform, like raising bid from low to high to hack compensation loopholes, or setting very high bid when budget is insufficient to hack braking loopholes. Therefore, the platform needs corresponding rules to avoid these problems, along with delivery guidance.

Besides bidding, advertisers also often hack the system by constantly copying plans. Because the ranking model often uses many ID features, this brings system variance issues. Two plans with identical delivery settings and creatives might have different delivery results due to different plan IDs, so advertisers have incentive to copy plans to get more volume. But this brings problems to the platform: (1) engineering pressure from more recalled plans or creatives (2) high creative repetition. This is also a creative ecosystem problem, and minor creative modifications belong to the same category. Therefore, the platform needs to consider problems from using ID features, or after using ID features, use additional strategies to ensure advertiser copying is ineffective, like managed control of client plan copying behavior, similar plan restriction and pruning strategies, similar creative identification, etc.

- Creator Ecosystem

Creator ecosystem, like client ecosystem, also needs to be examined by structure and industry. Because creator monetization is also a supply-demand business, we need to clarify supply-demand issues by follower segment or industry. For example, whether creator monetization follower distribution is healthy, whether only head authors monetize while most long-tail creators have no monetization at all. Industry-wise is similar, because content platforms want to increase content diversity, which requires increasing creator industry diversity since creators are an important supply of UGC platform creatives.

Besides the above issues, as mentioned earlier, content platforms often have “underwater” problems, meaning creator matching doesn’t go through official matching platforms but B reaches collaboration directly with K. This affects platform control over marketing content and platform revenue. This part will be expanded in the Creator section below.

- Content Ecosystem

In content ecosystem, besides red-line issues (like political, pornographic content), more ecosystem issues concern content diversity and content quality.

Content diversity issues were mentioned earlier, involving both client delivery content diversity and creator-created content diversity.

For clients, diversity issues manifest as clients not focusing on creative production but instead on various “tricks” like plan copying, leading to high creative repetition and user aesthetic fatigue. This negatively affects ad delivery user experience metrics and ad-related conversion rates long-term. To address this, the platform should provide guidance to get clients to focus on creative production. Ocean Engine’s Creative-Driven Delivery Platform does exactly this. Ocean Engine platform’s guidance for advertisers is also hoping advertisers drive business through creativity (image below from 2024 Ocean Engine Marketing Playbook).

For creators, diversity issues manifest as whether their content is sufficiently diverse. Generally, content diversity correlates with creator diversity, since each creator often has their own creative preferences. Therefore, the platform first needs to introduce sufficiently diverse creators, and can use mechanisms to influence creator creative tendencies, typically through opportunities and traffic - allocating more opportunities and traffic to creator types the platform wants to support.

Content quality is a very broad issue. Video shooting quality, content plagiarism, anti-intellectual content, strong marketing feel, etc. all count as content quality issues. These generally need identification and downgrading through review (human + machine). Additionally, creator matching often has “ghostwriting” problems, where creators aren’t genuinely sharing but directly publishing notes written by B (B does this to get more creators to endorse the brand, and creators only need to publish the written notes to get money). This not only easily leads to overall content having strong marketing feel, but also brings unhealthy atmosphere and phenomena in creator monetization, requiring platform mechanisms to suppress this trend.

Client

As mentioned earlier, clients have marketing needs on content platforms. To serve various client needs (cost, volume, low-barrier delivery, marketing objective diversity, data privacy, etc.), the platform needs to provide various delivery products. It also needs to deliver good delivery experience and results. Delivery experience is whether products can meet specific advertiser needs when they deliver on the platform, like ease of use. Delivery results also vary, most common being stable cost with maximum volume, along with volume stability requirements.

For delivery results, cost is the most fundamental and important part. Technically, CTR and CVR estimation accuracy is the basic guarantee (so unlike recommendation, ads generally have a calibration module for CTR and CVR objectives), with bidding and billing as fallback. This fallback mainly refers to handling CTR and CVR estimation inaccuracy, i.e., bidding will pace based on posterior conversions and spend to maintain cost. Besides bidding, during billing, the platform can also charge less or more based on current plan state. Bidding and billing, besides being fallback for CTR and CVR estimation inaccuracy, also alleviate the second-price difference from common second-price charging. I won’t expand on this here; see my earlier An Overview of an AD System.

Below I’ll mainly introduce related actions from the perspective of “platform wants clients to do long-term operations”.

Industry/Scenario-Based

Ad systems generally develop industry-specific optimization needs after reaching a certain scale. The reason is different industries have different marketing objectives and paradigms, making it hard to meet all advertiser needs with one unified solution. So industry-based optimization and recommendation is needed. Industry classification has many standards. Referencing Ocean Engine’s standard, there are mainly 4 scenarios/industries: e-commerce, download, local, and leads.

- E-commerce

E-commerce is generally divided into closed-loop e-commerce and traffic-driving e-commerce. The former is in-site conversion with merchant budget type; the latter is out-site conversion with merchant budget + platform budget types. Merchant budget marketing objectives are basically product purchases, store/livestream visits, etc. Platform budget basic objectives are new user acquisition or reactivation. Because budget types overlap, closed-loop and traffic-driving e-commerce have similar optimization objectives and paths, with two major differences:

Data completeness and timeliness. Since conversion happens off-site, traffic-driving e-commerce has worse data completeness and timeliness than closed-loop e-commerce, often requiring external data collaboration to get external data for modeling. Data security issues also arise, generally requiring privacy-preserving computation for cross-domain data interaction.

Universal delivery. Merchants doing traffic driving may not have their main operation site on the corresponding media platform (like merchants driving traffic from Douyin to Taobao, with main operations on Taobao). Such merchants generally won’t do daily content operations on Douyin (i.e., little natural traffic), and traffic-driving delivery evaluates whether ROI meets standards. But closed-loop e-commerce merchants have incentive to do content on the platform to get natural traffic. For these merchants, the industry has launched “universal delivery” products to let merchants better get natural + ad traffic.

- Download

Download is more accurately a conversion objective. Industries like gaming, web services, and e-commerce platform budgets all have download-type budgets. Gaming is the download industry that went deepest into optimization objectives earliest, from initial downloads to subsequent next-day retention, payment count, payment amount, etc. Gaming advertisers were the first to accept deep conversion objective optimization.

Making optimization objectives deeper, closer to advertiser marketing needs, is a process ad platforms must go through in evolving toward performance advertising. In this process, we often encounter problems where ROI improves but volume drops after switching from shallow to deep objectives. This requires weighing whether to accept short-term spend “loss” while bringing more value to advertisers, because only by serving advertisers well can the platform get sustainable revenue and growth.

- Leads

Leads is also a fairly broad concept covering many industries. Industries that need to provide services like real estate, automotive, education, and medical aesthetics all involve leads. Common methods like phone forms or private messages all count as leads, which are conversion objectives ad platforms need to optimize.

But leads face a problem of lead validity. Many customers who provide phone or send private message have low probability of subsequent conversion, which doesn’t bring actual conversion value to merchants. So deep lead conversion is also a persistent problem in the leads industry. The basic solution is to have more connection with advertisers, bringing more deep conversion data back to the platform side. Ocean Engine proposed a methodology as shown below.

Leads exist in many SMB industries (e-commerce too). In many service and goods selling industries, there are many small-scale businesses. These small merchants also have marketing intentions, but due to small budgets and insufficient delivery experience, they often face more problems. Some solutions for these will be mentioned in the SMB section below.

- Local

Local has significant overlap with the previous scenarios. Its major characteristic is services are geographically limited to a certain radius, and require store visits to provide services (similar to leads ads in this regard). Optimization methods aren’t much different from other industries (except needing some geographic restrictions).

KA and SMB

Based on business scale, budget, and other factors, clients can be roughly divided into KA (Key Account) clients and SMB (Small and Medium-sized Business) clients. The former often has sufficient budget and mature delivery capabilities, while the latter often has limited budget and less delivery experience. SMB client numbers are generally higher than KA clients.

But ad systems have Matthew effect where most money is spent by a small portion of advertisers. The reason is many long-tail SMB advertisers can’t compete well with KA advertisers due to weaker competitive ability and less delivery experience. These advertisers face further problems in delivery pipeline due to sparse data and insufficient model learning, further exacerbating this issue.

But the platform’s long-term revenue and CPM growth depend quite a bit on more intense competitive environment from increasing advertiser count. So SMB advertisers can’t be ignored by the platform. To serve these SMBs well, the platform needs to do specific optimization for them.

Two main problems bothering SMB clients are creatives and delivery. The former because clients aren’t professional content creators and can’t make good creatives, while often having no extra creative budget to buy good creatives. The latter due to unfamiliarity with platform rules and delivery processes, leading to high operation costs.

Therefore, platform delivery products for these SMB advertisers need sufficient ease of use, including providing more convenient delivery entry points and guidance, simplifying creation process, while providing automatic creative generation and editing capabilities to improve convenience for these advertisers.

Additionally, in traffic distribution, SMB advertisers with weaker competitive ability and lower eCPM can’t compete with KA advertisers. They often need platform traffic incentives and support, which may hurt overall platform spend because it breaks the revenue-maximizing distribution mechanism.

For leads industry SMB clients, Ocean Engine’s solution approach is basically what’s mentioned above, while also providing private message smart customer service.

E-commerce SMB solutions are similar.

Operations

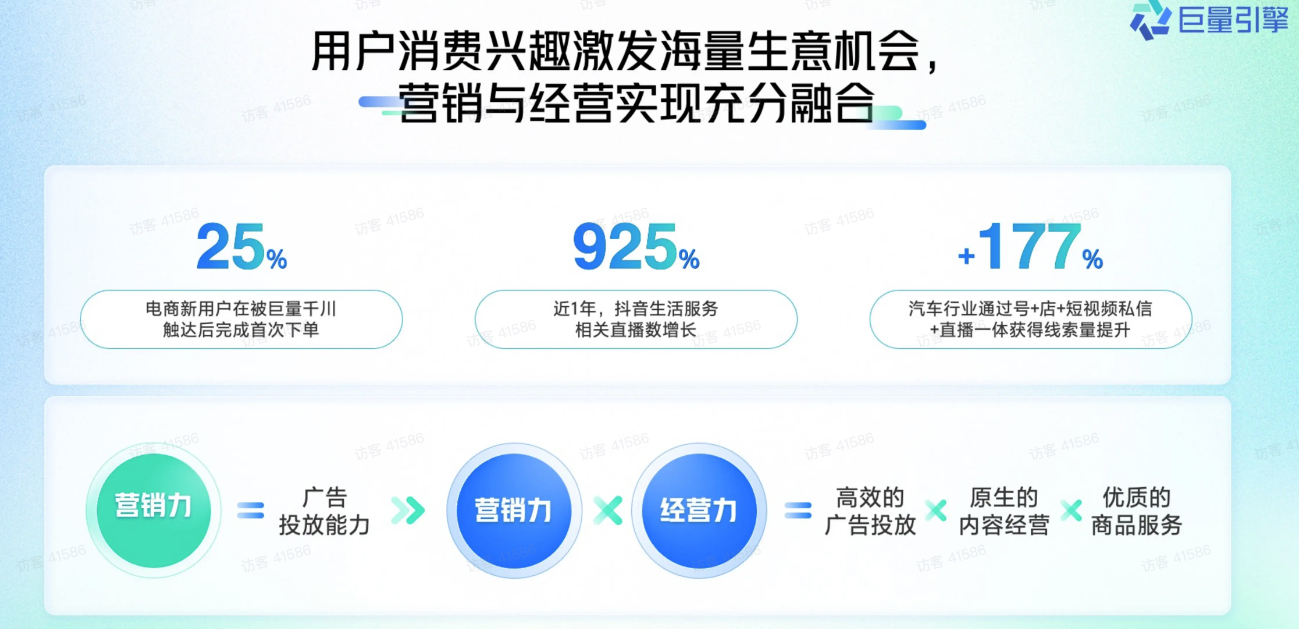

As marketing becomes more refined, platforms advocate clients shifting toward an operations direction during marketing. From client and platform perspectives, a more sustainable approach compared to just buying traffic through ads to reach users is using ads to pass cold start, then continuously attracting and retaining users through good content and good service.

Ocean Engine defines this as marketing capability (see below), meaning besides just spending money on ads, clients also need ability to make good creatives (to get more natural traffic) and ability to provide quality service (reputation guarantee, retaining users). This is a more sustainable development direction for both clients and platforms. This is also what I mean by “operations” in my understanding - using good content or money to get traffic (former is natural traffic, latter is ad traffic), then based on customers reached through this traffic, further expanding user base.

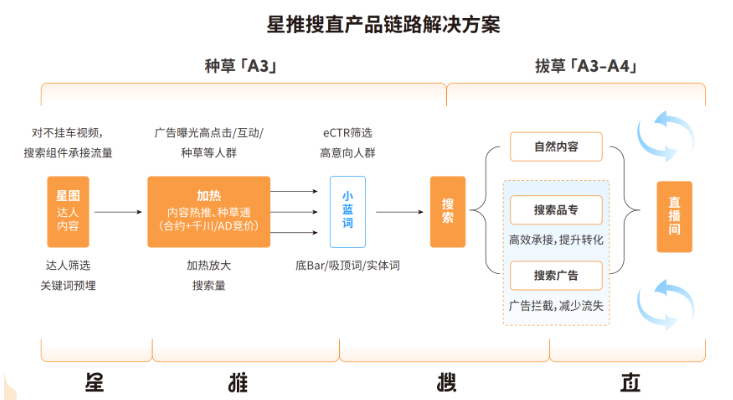

In this process, the platform needs to provide better methodologies and tools to guide advertisers, like Douyin’s “Star-Push-Search-Direct” methodology, Xiaohongshu’s KFS methodology, all guiding advertisers on how to better integrate platform-provided marketing capabilities, including creative production and delivery methodologies.

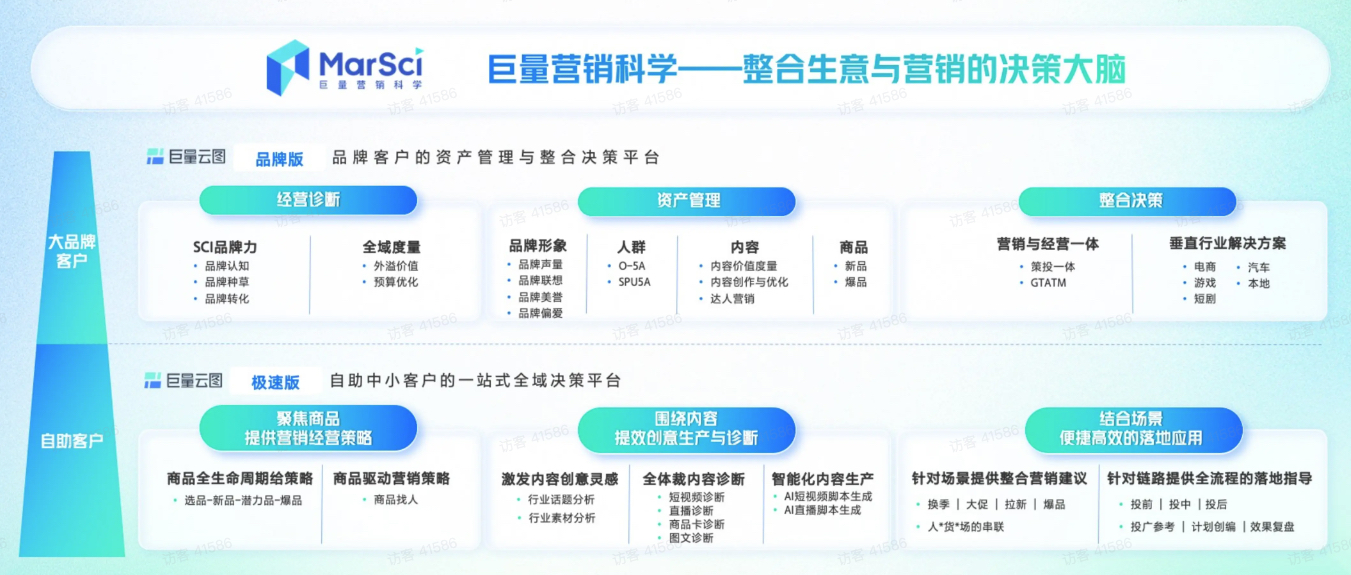

Besides methodologies, the platform also needs to provide corresponding capabilities and tools, like operation diagnostics, asset management (population assets like Douyin’s 5A population). See the diagram below for details.

Creator

Creators are an important source of platform quality content. To enable creators to continuously create good content on the platform, the platform often needs to provide two capabilities for creators: opportunities and heating. Opportunities are creator monetization matching opportunities, supported by platforms like Xingtu mentioned above. Heating is traffic-buying products for creators, an important tool for creator growth.

Opportunities

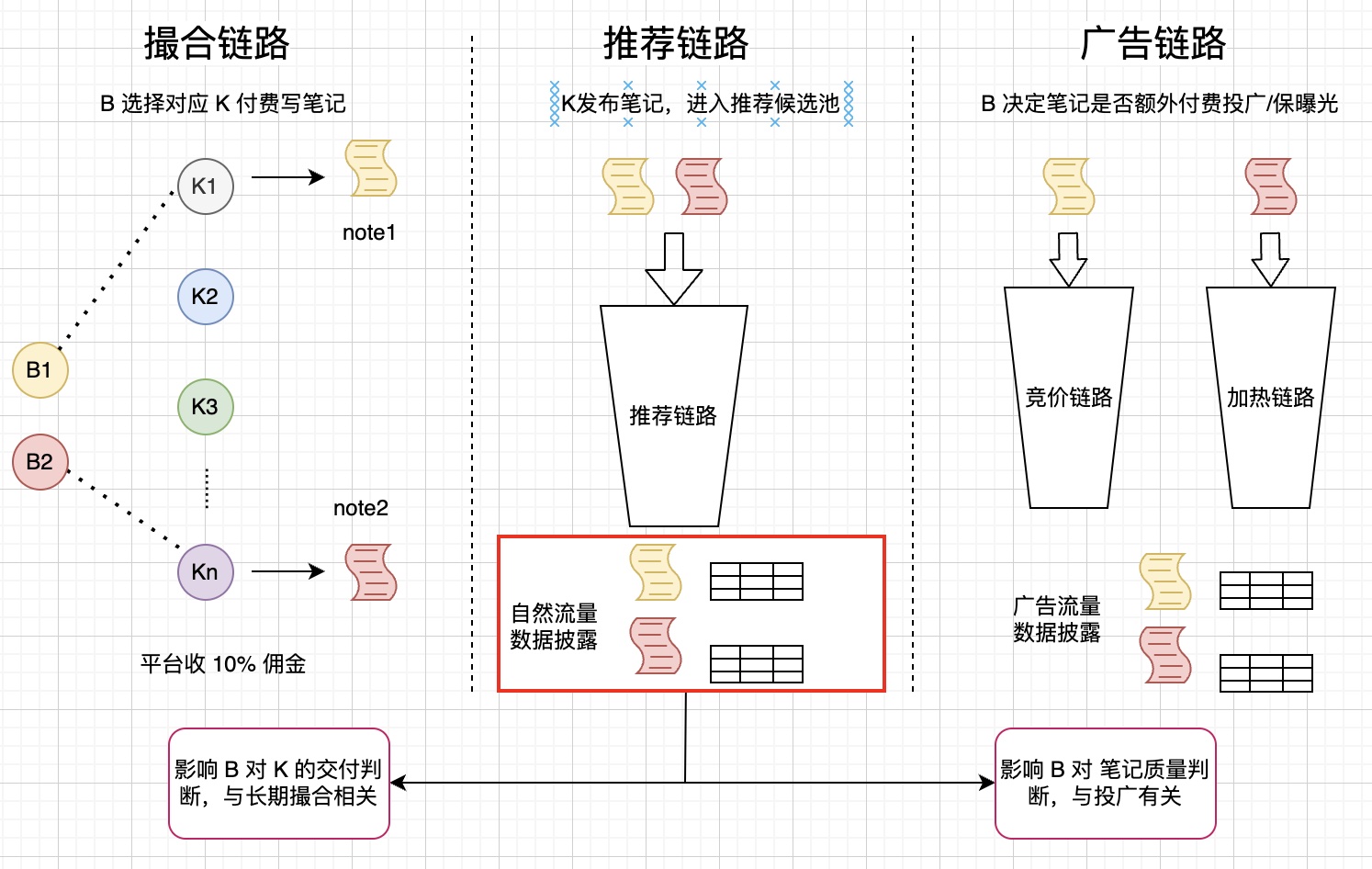

Colloquially, opportunities the platform provides for creators are B-K matching, i.e., B pays K to write and publish notes, buying K’s content and traffic.

Therefore, the platform needs to ensure completeness and ease of use of matching capabilities. Completeness means platform-provided matching capabilities need to cover basic paradigms. Common matching includes 1v1 precise mode, 1vN recruitment mode, with settlement methods including fixed-price and performance-based CPS settlement.

- 1v1 and 1vN

1v1 matching with fixed price is a basic mode, where B selects corresponding K on platform, pays for K to write and publish notes. 1vN and CPS settlement are more performance-based approaches, providing monetization opportunities for more mid- and long-tail K. The mode is generally B expresses needs, platform publishes needs to a group of K, then B settles based on actual results (like impressions, likes) from notes created by K. Compared to 1v1, this mode allocates B’s budget from one K to multiple K. Xingtu’s Publisher Program is a typical 1vN mode.

- Above-water and Underwater

These official matching platforms often face the problem of budget going “underwater”. Let me explain a concept: above-water means B-K matching through official collaboration platform, requiring commission payment to platform. Underwater means B directly connects with K without going through platform.

From platform perspective, it definitely wants B-K matching to go above-water, because besides commission, it can have better control over this type of opportunities. But from B’s perspective, going underwater saves commission and makes content more native (some platforms explicitly mark above-water content), so underwater vs above-water gaming will be a long-term problem the platform needs to solve.

To get more budget from underwater to above-water, the platform needs to do two things well:

Improve matching platform ease of use and efficiency, i.e., platform needs to make B-K connection easier.

In traffic distribution, above-water needs differentiated distribution mechanism from underwater, and reveal benefits of above-water to B-side.

Point (1) is mainly related to matching pipeline. Point (2) is strongly related to the recommendation pipeline mentioned here, because B-K matched notes are basically no different in form from notes K publishes themselves, generally going through general distribution. In this approach, above-water and underwater notes have no difference in traffic distribution, so B has less incentive to go above-water.

So to convert underwater to above-water, above-water traffic distribution needs to be differentiated, considering more B-side benefits. Actually, K and B’s benefits/objectives aren’t binary opposites - fundamentally the platform intervenes in allocation of B’s money among different K. So first serve B willing to pay, then consider how to allocate well among different K.

B-side generally has marketing needs. Creatives bought on platforms like Xingtu and Pugongying are an important source of their ad creatives. The natural traffic effect after K publishes is a key factor affecting whether B uses this creative for advertising. As shown below, in B’s money-for-“creative+traffic” mode, the recommendation pipeline’s natural traffic affects efficiency in both front and back pipelines.

Therefore, differentiated traffic distribution refers to this natural traffic distribution method and effect. In practice, we can consider adding some B-side marketing objectives as part of the ranking formula for this traffic, while doing proper attribution and revealing to advertisers for this traffic.

Ad Pipeline

As mentioned earlier, advertisers will use B-K matched creatives for advertising. In practice, we often observe this phenomenon - using B-K matched creatives for advertising yields better results. Reasons are often as shown below from Xingtu statistics (from 2024 Ocean Engine Marketing Playbook).

And an important basis for deciding whether to advertise content is these creatives’ performance on natural traffic. From technical perspective, these two traffic distributions are independent pipelines with different distribution objectives, so there’s a problem of weak traffic correlation, making traffic data less valuable for B-side advertising decisions. Simply put, if a client uses a note with good natural traffic data for advertising, actual ad performance might not be good. Clients lack methodology for choosing creatives to advertise.

From technical perspective, one direction for technical work is strengthening correlation between natural and ad traffic, i.e., making clients feel these two traffic sources are correlated. Because this natural traffic for advertising creatives is somewhat like cold start traffic for note advertising. Better utilizing this cold start traffic to assist client advertising can potentially drive growth in both matching transaction volume and ad transaction volume.

In specific technical approaches, as mentioned earlier, we can add some B-side marketing objectives in recommendation pipeline distribution as ranking formula terms. On this basis, sharing features/samples between these two traffic sources can strengthen ad cold start effects. For creatives performing well on natural traffic, when used for advertising, we can also try more aggressive ad bidding strategies.

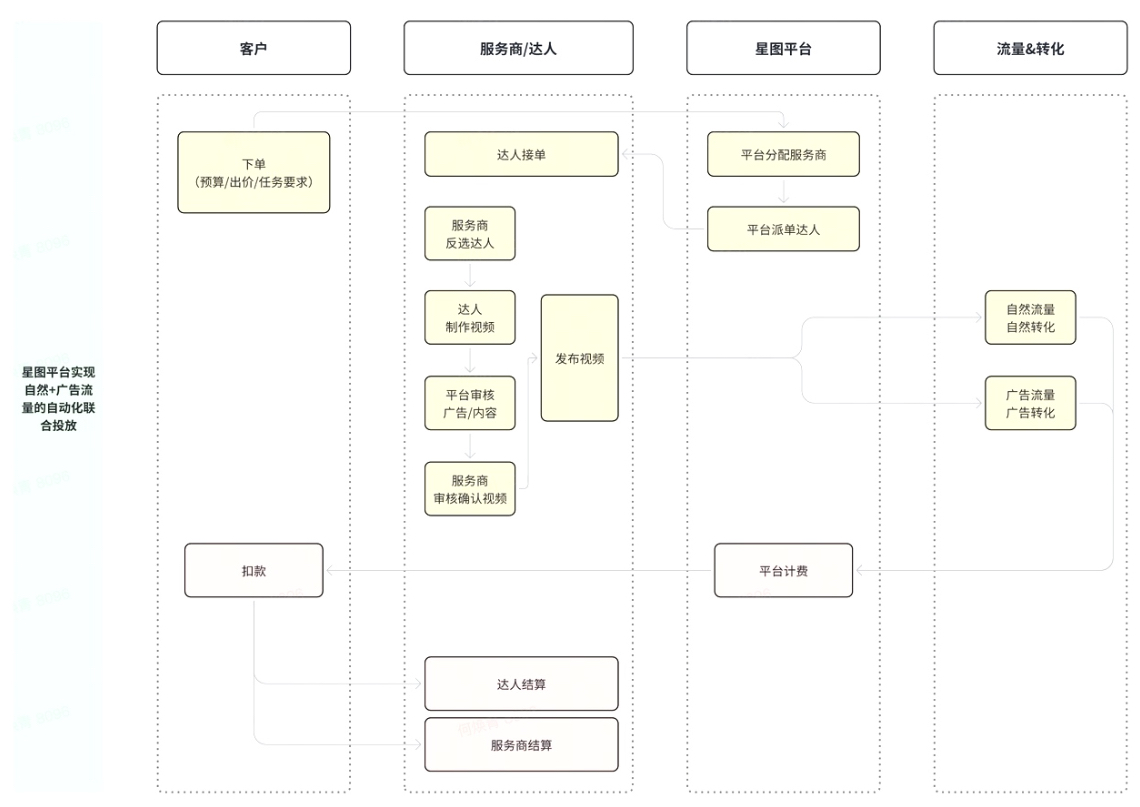

The most extreme linkage is products like Xing-Guang Joint Delivery. This product no longer follows the sequence of natural traffic first, then ad traffic, but uses client budget to do marketing on both natural and ad traffic simultaneously, as shown below.

Heating

Heating often complements opportunities. Heating is a paid tool creators use to assist their growth. After growing to a certain follower volume, they need opportunities to monetize. It’s somewhat like B-side perspective of planting and harvesting.

dou+, Fentiao, Shutiao and similar products are content heating tools serving all creators.

These products have requirements for creator content quality, often requiring not too strong marketing feel, with dedicated content review, and no marking. “Heating” also means weak optimization objectives, generally reading, likes/saves, profile visits, follows, etc., relatively shallow objectives.

Meanwhile, dou+ also supports strong marketing objectives like customer acquisition, product purchases, livestream promotion, etc., as shown below. A major difference from the shallow marketing objectives mentioned earlier is who it serves. Heating generally serves creators, with main objective being their own growth. Strong marketing objectives serve advertisers with strong creative production capabilities. This advertising generally still evaluates cost, ROI, etc. This also relates to the traffic mechanism mentioned below.

Bidding and Budget

Because creators have limited understanding of ad bidding, they often choose nobid-type bidding to lower the barrier for understanding cost-based bidding like cost and compensation. There’s an interesting question here - viewing budget growth logic for various products from bidding perspective.

First, cost-based bidding like oCPX. Budget growth logic is through bidding, models, etc. optimization to make actual conversion cost closer to advertiser bid. Then as overall competitive ability strengthens and overall eCPM level rises, advertisers need to raise bids to get more volume. This is equivalent to advertisers willing to pay more for a conversion, platform selling conversions more expensively, driving overall revenue growth (with same conversion count).

nobid bidding can generally spend all budget. So nobid budget growth is often about lowering conversion cost, improving advertiser ROI, then advertisers willing to invest more budget.

nobid cost needs to continuously decrease, which seems contradictory to cost-based bidding mentioned earlier. From long-term overall spend growth perspective, adload, CTR, CVR all have upper bounds, meaning conversion count is limited. So continuously lowering conversion cost is equivalent to continuously lowering overall revenue.

Therefore, we can’t let nobid-type bidding product costs continuously decrease. The “advertiser ROI improves, then willing to invest more budget” mentioned earlier is a relatively long-term budget growth logic. In this process, costs often rise. For example, two nobid plans with identical configuration except budget - in this configuration, the higher-budget plan often has higher cost than lower-budget, because cheap traffic is limited in a period’s traffic pool.

So the problem becomes: when advertisers raise budget in nobid products, bringing simultaneous cost and volume increase, whether cost is still within advertiser’s expected ROI red line. If yes, they might accept cost increase. Therefore, nobid spend growth logic becomes: platform continuously optimizes advertiser cost through efficiency optimization, attracting advertisers to increase budget (within acceptable cost range), driving overall spend growth (since nobid budget can always be spent).

This way, nobid growth logic is similar to oCPX - selling conversions more expensively within advertiser’s acceptable range. The difference is raising bid in oCPX becomes raising budget in nobid.

Traffic Mechanism

Since heating products are essentially platform selling traffic (like advertiser products), in traffic distribution, a straightforward approach is competitive bidding between unmarked content and marked ads - i.e., ranking based on eCPM mixed competition with ads, same mixed ranking constraints, sharing ad load with ads.

But this reveals a phenomenon: once big promotions like 618 or Double 11 occur, under mixed competition, these heating products’ load decreases, while various marketing objective conversion costs rise.

The root cause is under mixed competition, this heating content competes for traffic with ads, so costs rise and fall with ad bidding overall cost level, unable to achieve relatively low costs. Creator budgets are small, bidding ability weak, so under mixed competition with large advertisers, they easily get squeezed by large advertisers. Or content quality + unmarked advantage in CTR/CVR can’t compensate for bid disadvantage.

Therefore, this type of unmarked paid heating content (some platforms call native ads) often needs independent ranking pipeline and load, while needing independent constraints in mixed ranking (first slot, minimum gap), or as one lane mixed with hard ads and recommendation content, avoiding being too severely squeezed by hard ads.

To some extent, this is a traffic value depression. Because creator heating products also bear ecosystem value of creator growth and enriching platform content, so this traffic is also a form of support for creator growth.

Self-Delivery and Proxy Delivery

Generally, creator heating products are self-delivery or proxy delivery, i.e., creators pay out of pocket to heat their own work, or creator fans voluntarily pay to heat creator notes. Overall budget is generally small, easily squeezed by large advertisers.

But there’s a slightly different proxy delivery mode, where platform selects UGC notes for large advertisers, then large advertisers heat these UGC notes. For example, taking Genshin Impact game - there are many UGC notes. Platform intermediates through “matching” to let advertisers willing to heat these UGC notes. Intuitively, this seems like a win-win-win model:

- For users, as long as they create good content, they have opportunity to be selected by platform and advertisers, receiving traffic subsidies (brand paid) and cash subsidies (optional).

- For advertisers, saving creative production costs. Platform selects notes with weaker marketing feel from massive UGC notes for brand delivery.

- For platform, able to introduce more budget this way (possibly transfer), while using brand money to assist creator growth.

But the product itself has limitations:

- Basically only suitable for large brands/advertisers, because brand needs to be well-known by users to have many UGC notes.

- If large brands can spend budget well this way, they might not buy creatives on matching platforms anymore, potentially affecting matching transaction volume.

In technical implementation, overall not much different from conventional heating. Main difference is involving note selection process, including pre-delivery selection and mid-delivery optimization. Because UGC note count is generally large, how to algorithmically select appropriate notes for brand to choose for delivery, or make managed optimization during delivery, is a problem to consider.

Summary

This article mainly discusses two things related to creators: opportunities and heating. The former is how creators make money, the latter is how creators spend money for growth.

Platform-launched matching products are important tools for completing opportunities. A complete lifecycle often involves three pipelines: matching, recommendation, and ad pipelines. Among them, traffic distribution in recommendation pipeline is particularly important, because it simultaneously affects B’s judgment of K’s note quality and subsequent advertising decisions, thereby affecting matching transaction volume and advertiser advertising budget, etc.

Platform-launched heating products are important tools assisting creator growth. This article explores common nobid-type bidding budget growth logic for these heating products, traffic mechanism, and a new proxy delivery product form. In this process, the platform needs to fully exercise initiative, especially for traffic mechanism, not considering this traffic’s value only from revenue perspective.